Logistics rents across Asia-Pacific held nearly flat in the first half of 2025, dropping just 0.4 percent year-on-year despite global trade tensions and heightened caution among occupiers, according to Knight Frank’s Logistics Highlights H1 2025 report. This represents the first year-on-year drop since 2020, when the pandemic triggered a surge in demand for logistics spaces. Key regional insights include:

Overall Stability, Emerging Divergence

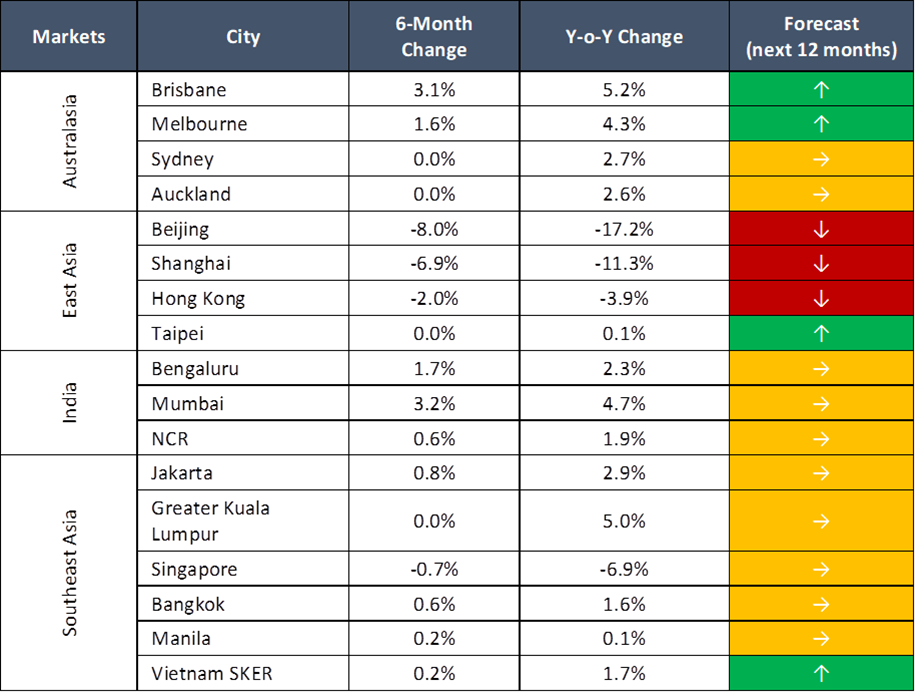

While rents in Chinese mainland markets continued their downward trajectory, momentum for rental growth in Australia and Southeast Asia slowed considerably. Most other regional markets registered modest gains, keeping the broader rent index in stable territory.

India posted the strongest growth in the Asia-Pacific logistics sector. The country’s manufacturing sector hit a 14-month high with its S&P Purchasing Managers’ Index reaching 58.4 in June, the strongest performance across the region, driven by rising international sales, higher output, and record-breaking employment growth. Despite a rise in vacancies across India’s three largest logistics markets, rents climbed at a faster 3.4 percent in H1 2025, up from 2.1 percent six months ago. This outperformance was driven by sustained demand from the manufacturing sector, which remained the most prolific occupier group and continued to anchor the market.

Brisbane led all regional markets in rental growth, with rates climbing by more than 5 percent annual rental growth in H1 2025. Despite this, the city has seen its vacancy levels climb above long-term averages, leading landlords to offer higher incentives to fill speculative new supply. With new development set to slow after 2025, the market is expected to stabilise.

Companies See an Opportunity to Reposition Logistics Portfolios

Much of the region’s stability in H1 2025 may also reflect strategic front-loading of shipments ahead of tariff deadlines, raising questions about occupier demand in the coming months. Companies are now reassessing costs and operational flexibilities to optimise their logistics portfolios.

Tim Armstrong, global head of occupier strategy and solutions, Knight Frank, explains, “As firms weigh their strategic priorities, real estate portfolios are increasingly being reconfigured to support more resilient, regionalised supply chains. This includes investment in distribution hubs, proximity to ports or multimodal transit networks, and the integration of logistics infrastructure with office and support functions.

Occupiers are likely to focus more resources towards establishing bigger and more efficient logistics hubs close to urban areas while right-sizing those in less strategic locations. This trend is already evident in Australia, where occupier demand has gravitated towards prime areas, such as Brisbane’s Trade Coast. As rental growth in the region continues to moderate, the current window represents an opportunity for occupiers to strategically position their portfolio for long-term growth.”

Chinese Mainland Shows Signs of Stabilisation

Chinese mainland markets, which have been under pressure, showed encouraging signs of recovery. Rental declines moderated significantly to 12.8 percent year-on-year from 14.1 percent in H2 2024, supported by government stimulus measures that boosted demand for digital devices and logistics services. Total stock in Beijing and Shanghai reached approximately 20 million square meters, though vacancy rates climbed to 27.3 percent. In Hong Kong SAR, a healthy supply pipeline through 2027 is expected to keep rents under pressure, even as leasing velocity remains subdued.

Looking ahead, Shanghai is expected to see narrowing rental declines in late 2025 as supply peaks pass, though Beijing faces continued pressure with an additional 2 million square meters scheduled for delivery in H2 2025.

Chistine Li, head of research, Asia-Pacific, Knight Frank, says, “While rents have continued to dip in Chinese mainland markets, further deceleration across the rest of the region have dragged rental growth into negative territory. We believe this to be largely due to occupier caution, as there has not been a significant deterioration in the region’s fundamentals. As occupiers explore relocations or dual logistic strategies to mitigate cross-border tariff risks, India, with a more competitive tariff structure as well as lower costs, is emerging as an important node in China-plus-n strategies. Occupiers in the region can be expected to remain agile in adapting and evolving their supply chain strategies to weather the shifting geopolitical landscape. While expansion plans will be put on hold, we expect selective demand to remain sustained in emerging Southeast Asian markets and India.”

Market Outlook and Strategic Implications

Although conditions in logistics occupational markets in the region have remained stable so far, part of this stability may be attributed to the frontloading of shipments ahead of tariff deadlines, as occupiers strategically advance inventory to avoid additional costs. As the effects of these pre-emptive moves taper off, the region is likely to see a period of recalibration.

The increasingly complex dynamics, ranging from shifting supply chains and evolving geopolitical tensions to fluctuating trade policies, will continue to weigh on occupier activity in the latter half of the year. Businesses are expected to reassess their logistics footprints, weighing the imperative to control costs against the need for operational efficiency and the pursuit of long-term growth opportunities

Forecast for the Next 12 Months