https://brj.com.sg/wp-content/uploads/2015/04/pentair1.png

477

372

Editorial Staff

Editorial Staff2015-05-04 16:31:312015-10-11 04:32:52Making an energy-efficient splash

https://brj.com.sg/wp-content/uploads/2015/04/alami2.png

306

449

Editorial Staff

Editorial Staff2015-05-04 15:33:062015-05-05 11:16:56Maintaining ideal thermal comfort yet saving energy

https://brj.com.sg/wp-content/uploads/2015/04/indoor_office_hvac_system.jpg

615

900

Editorial Staff

Editorial Staff2015-05-04 15:20:032015-05-05 11:18:46Your Building’s Indoor Environment Affects Your Worker’s Productivity

Clean and Renewable Energy

Reading Time: 6 minutes

While Europe still represents a major part of all installations globally, Asia’s demand started to grow rapidly in 2012 and this growth was confirmed in 2013. It reached 59% of 2013 installations while Europe went down from 82% in 2010 to 28% in 2013.

Solar Photovoltaic (PV) is perhaps the first thing that comes to people’s minds on the subject of clean renewable energy. PV technologies convert energy from sunlight into direct current (DC) electricity. They provide an ideal sustainable energy solution for remote rural areas, where it is neither technically feasible nor economically viable to extend grid coverage to isolated areas. However, in developed urban cities, it is common to find PV systems installed in buildings and on rooftops as well.

Globally, PV demand has been on an upward trend. Especially in recent years, the demand accelerated as the price of the commonly-used PV material – crystalline silicon – took a plunge from $4/watt in 2008 to $2/watt in 2010. Today, it even costs less than $1/watt, and observers foresee that the prices will fall further. The sharp drop in prices is largely due to innovations in PV technologies and manufacturing automation. This price movement stands in contrast with the rising cost of electricity as fuels are being depleted.

The growing preference for choosing sustainable solutions has also egged on the PV market. This is due to a combination of reasons such as the on-going global struggle to reduce carbon emissions, government incentives, schemes to encourage green building, and higher capital value for buildings with green certification.

An Overview of PV Technology

In general, PV materials are mainly categorized as crystalline silicon(c-Si) or thin film. They are judged on two basic factors – efficiency and economics – to determine which application is best. These materials are further subdivided into different categories which provide different efficiencies.

Crystalline silicon (c-Si)

Monocrystalline silicon Panel

Multicrystalline silicon Panel

For remote installations where the space available for PV panels is often quite limited, the greater conversion efficiency of c-Si technology has the advantage. C-Si modules represent 85-90% of the global annual market today.

C-Si modules are subdivided into two main categories: single crystalline silicon (Sc-Si) and multi-crystalline silicon (mc-Si). Sc-Si panels should be used when a higher voltage is desirable. This would be when the DC power has to travel some distance before being utilized or stored in a battery bank. These panels are also the most efficient in PV technology, averaging 14% to 17% efficiency. In comparison, mc-Si panels have efficiencies of 12% to 14% but they can often be purchased at a lower cost per watt than sc-Si panels.

Thin film technology

While thin film panels are cheaper than c-Si panels, it is worth noting that the conversion efficiency of thin-film panels is lower and tends to drop off rather rapidly in the first few years of operation.

Thin films are subdivided into three main families: amorphous (a-Si), Cadmium-Telluride (CdTe), and Copper-Indium-Gallium-Selenide (CIS/CIGS). Depending on the technology, thin-film module prototypes have reached efficiencies of between 7–13% and production modules operate at about 9%. Performance deterioration must be taken into account when assessing the array for a multi-year project. However, there are still applications where the lighter weight and greater flexibility of the thin-film panels may be more suitable. Thin films currently account for 10% to 15% of global PV module sales.

Types of PV Systems

There are different types of systems in which the PV modules are integrated. Solar PV systems are mainly divided into grid-connected / grid-tie systems and off-grid / stand-alone systems.

For grid-connected systems, the PV system operates in parallel with the public electricity network. In general, most of the PV systems installed in developed countries are grid-connected.

If connection to the grid is not possible, or if there are no electricity mains, then the PV systems are installed as stand-alone systems.

Thin film technology

While thin film panels are cheaper than c-Si panels, it is worth noting that the conversion efficiency of thin-film panels is lower and tends to drop off rather rapidly in the first few years of operation.

Thin films are subdivided into three main families: amorphous (a-Si), Cadmium-Telluride (CdTe), and Copper-Indium-Gallium-Selenide (CIS/CIGS). Depending on the technology, thin-film module prototypes have reached efficiencies of between 7–13% and production modules operate at about 9%. Performance deterioration must be taken into account when assessing the array for a multi-year project. However, there are still applications where the lighter weight and greater flexibility of the thin-film panels may be more suitable. Thin films currently account for 10% to 15% of global PV module sales.

Building Integrated Photovoltaics (BIPV) System

Building Integrated Photovoltaics (BIPV) is the integration of PV into the building envelope (eg. windows, walls, or roof tiles etc). It allows for seamless integration into a building’s design. BIPV products work particularly well for new building construction or a significant remodeling. The PV modules serve the dual function of being the building skin – replacing conventional building envelope materials – and power generator.

BIPV systems should be adopted where there is energy-conscious design, and where equipment and systems have been carefully selected and specified. They should be viewed in terms of life-cycle cost, and not just initial, first-cost. The overall cost may be reduced by the displacement of inefficient building materials and labor. Design considerations for BIPV systems must include the building’s use, its electrical loads, its location and orientation, the appropriate building and safety codes, and the relevant utility issues and costs. However, as BIPV panels are made for both photovoltaic and thermal collection systems, designers often place both technologies side-by-side to further maximize efficiencies.

Evolution of PV Demands

According to a report[1] “A Snapshot of Global PV 1992-2013” by International Energy Agency (IEA), preliminary market data shows that there is a growing market in 2013, for the first time in two years. At least 36.9 GW of PV systems have been installed and connected to the grid in the world last year. While these data will have to be confirmed in the coming months, some important trends can already be discerned:

- The global PV market grew to at least 36.9 GW in 2013, compared to around 29 GW in the last two years.

- Asia ranks in first place in 2013 with more than 59% of the global PV market.

- The market in Europe has decreased significantly from 22 GW in 2011 to 17 GW in 2012 and 10.3 GW in 2013. For the first time since 2003 Europe is no longer the top PV market in the world.

- The Asian markets experienced the highest growth (+170%) and China took first place (with an estimated 11.3 GW of grid connected PV systems), ahead of Japan (6.9 GW1) and the USA (4.75 GW). The first European country ranked fourth, with 3.3 GW installed is Germany.

- In the top 10 countries, 4 are Asia-Pacific countries (China, Japan, India, Australia)

“Asia ranks in first place in 2013 with more than 59% of the global PV market.”

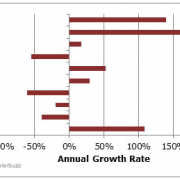

The top 10 global PV markets alone accounted for over 80% of end-market demand in 2013. Looking at last year’s growth rates of these countries in 2013, it shows a distinct trend that end-market demand is shifting away from Europe and towards Asia. In fact, the three fastest growing markets in 2013 were Japan, China, and Thailand, each more than doubling their end-market demand levels over the previous year. Conversely, three of the top European markets saw end-market levels decline in 2013, with only the United Kingdom showing growth.

![Top 10 global PV markets of end-market demand in 2013 (Figure by NDP Solarbuzz – Marketbuzz 2014 report[2])](https://brj.com.sg/wp-content/uploads/2015/04/graph.png)

Top 10 global PV markets of end-market demand in 2013 (Figure by NDP Solarbuzz – Marketbuzz 2014 report[2])

China has announced the installation of 11.3 GW of grid-connected PV in 2013. According to Chinese figures, the installations could have been even higher than that but some uncertainty remains on whether these additional PV systems have been connected to the grid or not. In any case, Chinese PV installations have set a new record in terms of new installations, above the 9.3 GW reported in Italy in 2011. This performance is in line with the ambitions of the Chinese authorities to continue developing the internal PV market, pushing for 35 GW by the year 2015 and 100 GW by 2020.

Japan was the second market for PV in 2013 with an estimated 6.9 GW of PV installations. While final numbers could slightly differ, this shows a dramatic increase in both countries compared to 2012.

In Asia, after the two market leaders, Thailand continued to grow, with 317 MW installed in 2013 and 704 MW of total capacity. Other markets continued to grow at a slower rate, such as Taiwan (170 MW), Malaysia for the second year of its feed-in tariff system (42 MW), as well as a few others.

Asia is undoubtedly the new focal market for PV.

https://brj.com.sg/wp-content/uploads/2015/04/solarfarm.png

310

616

Editorial Staff

Editorial Staff2015-04-24 17:48:162015-04-24 17:55:38Solar PV Systems bring green energy for buildings

Be a step ahead with superior energy efficient solutions

Reading Time: 5 minutes

Buildings are valuable assets but the costs of maintenance can affect the bottom line of a business. As energy

costs continue to rise, building owners and facility managers face increasing pressure to reduce operational

costs, at the same time, increase productivity, improve sustainability and ensure business continuity for their

organizations.

A building’s chiller plants typically consume the most energy, so it makes sense that any strategy to reduce costs and to be environmentally friendly needs to start here. Johnson Controls is a global multi-industrial company with established core businesses in the building and automotive industries. It leverages on decades of YORK chiller innovations to deliver more efficient and sustainable chiller solutions in its continual push of the boundaries of chiller technology.

Larry Kouma

Product Management Director,

Asia Chiller Solutions, Johnson Controls Inc.

With over 20 years of experience in the HVAC industry, Larry boasts

vast technical knowledge in the design and application of steam and

chilled water systems. He is passionate about driving sustainability

across the value chain and has spent over a decade working with

energy efficiency standards. In addition, he has served on the

ASHRAE-ANSI 90.1 Standard Committee for 8 years.

In a recent interview, Mr. Larry Kouma (Product Management Director) shared his insights into regional trends in Asia’s refrigerant industry and on how the YORK® Magnetic Centrifugal Chiller (YMC2) system addressed the most pressing concerns of facility owners and designers.

BRJ: What are the regional trends in the refrigerant industry in 2014?

LK: With the awareness of ozone depletion and commitment to the Montreal Protocol, major suppliers are responding to the phase out of hydrochlorofluorocarbons (HCFCs). However, meeting all the requirements of safety, reliability, efficiency, Ozone Depleting Potential (ODP) and Global Warming Potential (GWP) is a tall order. The refrigerant that best fulfils these requirements are the hydrofluorocarbons (HFC) for large HVAC equipment applications, and in certain applications, natural refrigerants including hydrocarbons, ammonia, and carbon dioxide (CO2), are also safely applied.

BRJ: In what direction would these trends change in the next few years?

LK: Increasingly, refrigerants are also assessed based on their Life Cycle Climate Performance (LCCP), which takes a holistic approach in estimating all warming impacts – both direct and indirect – over the lifetime of the refrigerant for specific applications. Research will continue to push forward to find or create refrigerants that best fulfil all the necessary criteria while minimizing climate impact. Meanwhile, HFCs look to be the mainstay with European Union F-Gas Regulation to mitigate its GWP by addressing the containment, use, recovery, reporting, labelling, training, certification and some market prohibitions. This will have implications especially for sectors with high leakage such as automotive and commercial refrigeration.

BRJ: What are some of the most pressing building and facility challenges faced in the industry today?

LK: Rising energy costs and the need to improve productivity and minimize downtime continue to be key challenges for building and facility managers today. In addition, there is growing interest in sustainability across the industry as organizations increasingly seek to incorporate it into business goals and culture.

With the increased focus on climate change globally, many countries are enacting legislation and providing

incentives to modernize and retrofit existing facilities. In fact, the recent 2013 Energy Efficiency Indicator (EEI)

study by Johnson Controls found that such government policies and programs were one of the key drivers for

Asia to adopt “greener” and more energy efficient HVAC equipment and solutions.

In Singapore, the government’s push to green 80 percent of all buildings by 2030, mean that building owners

and facility managers will increasingly look to proven and reliable HVAC and solutions to help them to achieve

their energy efficiency and green building targets in the next few years.

BRJ: How does YMC2 help address them?

LK: Johnson Controls is one of the first to apply the magnetic-bearing technology to chillers, originally in response to mission-critical needs of the navy. Subsequently, we then extended this technology to make it available to other sectors (including commercial) to help address the growing demands with energy consumption reductions and sustainability. The magnetic-bearings reduce friction and vibration, while eliminating the need for oil to lubricate the bearings – delivering energy-efficiency, high reliability and noise control as a result. It addresses these challenges through:

Improved Efficiency – YMC2 chillers is 10 percent more efficient than new conventional, variable-speed chillers. The magnetic-bearing technology eliminates mechanical-contact losses in the driveline. In addition, proven energy efficient YORK® features such as the OptiSpeed™ variable-speed drive and the optimized centrifugal compressor have been retained and improved on. The efficiency benefits can be greater than 30 percent when considering replacement of an older existing chiller at end of life.

Reduced Noise – The YMC2 chiller is quieter than any water-cooled centrifugal or screw chiller on the market. Driveline vibration is eliminated with the magnetic-bearing technology, while the YORK® OptiSound™ control further helps reduce noise. As a result, the YMC2 chiller operates at a maximum of 73 dBA at full-load standard conditions (The human ear would perceive the YMC² chiller only half as loud as other magnetic-bearing chillers).

High Reliability – The design of the YMC2 chiller has fewer moving parts, requires less servicing and has a longer motor life. This helps to increase reliability and reduce maintenance costs. The chiller’s permanent-magnet motor has an inherently longer life than traditional motors, and the OptiSpeed drive’s soft-start sequence helps to further extend motor life.

Better Sustainability – The YMC2 chiller uses refri-gerant HFC-134a which has zero ozone-depletion potential. Furthermore, it is designed with 57 percent less refrigerant-piping connections which drastically reduce the potential for direct global warming caused by refrigerant leakage potential. The 10 percent to 50 percent efficiency improvement also reduces indirect global warming caused by greenhouse-gas emissions generated by electric utilities. Indirect impact is typically more than 95 percent of the chiller contribution to environmental warming impact over the operating life of the chiller.

BRJ: What is the potential for adoption of the new YMC2 technology in Asia?

LK: We see lots of potential for adoption in both the developed and developing markets in Asia. Interest in the developed markets, such as Australia, Hong Kong and Singapore, would be more immediate and widespread. For one, the YMC2 chiller is ideal for retrofit installations because it not only delivers higher efficiency but also caters to a higher capacity within a small footprint.

We are also starting to see interest in developing markets, such as India and China, where a few forward thinking companies have started to implement high efficient systems and solutions. At the same time, the governments in these countries have increasingly taken steps to drive the adoption of more energy efficient and green solutions across businesses and infrastructure through regulations and incentives. So we can expect good growth in these markets in the coming years.

In general, YMC2 is a versatile solution that is suitable for application across a wide range of industries. Given its high reliability and superior sound control, it is also recommended for high performance facilities such as data centers, healthcare facilities, educational institutions and concert halls.

BRJ: In terms of cost savings, how long is the payback with YMC2 installed?

LK: Generally less than five years, and can be lower than three years depending on total system design and ambient conditions.

BRJ: Does YMC2 help existing buildings? Please elaborate.

LK: The YMC2 contributes towards helping reduce the energy consumption and operational costs of commercial and industrial buildings. It is also ideal for retrofit in existing buildings because of its small footprint – it can fit into the old chiller space and still cater to a higher capacity (up to 560TR) and deliver higher efficiency. Its energy efficient and sustainable features also help existing buildings meet the energy management and environmental targets set out by building owners and increasingly, governments.

In Singapore, government legislation and incentives play a big part in driving the adoption of more energy efficient HVAC solutions. This is in part due to the Government’s push to green 80 percent of all buildings by 2030.

New regulations increasingly require new and existing buildings to achieve a minimum Green Mark standard when retrofitting or installing a new cooling system. Existing buildings are also required to carry out regular energy audits and report annual energy consumption data.

Johnson Controls, has helped existing buildings such as PoMo, a mixed-use retail facility achieve the BCA Green Mark Platinum rating with YMC2. The YMC2 helped address the needs of the building owners by reducing energy consumption and controlling excessive equipment noise. With the YMC2, the retrofitted chiller plant achieved an impressive system efficiency of 0.65 kW/RT and successfully lowered sound levels below 73 dBA.

A peek into Vietnam’s green adoption

Reading Time: 5 minutes

A recently published white paper titled “Is There a Future for Green Buildings in Vietnam?” assesses the current market overview of Vietnam’s green building industry. The document was released by Solidiance – an Asia-focused B2B management consultancy firm – in partnership with Vietnam Green Building Council (VGBC).

According to the paper, the green buildings market in Vietnam is still at the early stages of development, primarily as a result of cost sensitivities, low electricity prices, short-term thinking and misaligned incentives between building developers and users, an underdeveloped regulatory market, and a limited supply of skilled employees with green building awareness.

At present, there are only approximately 40 buildings that have achieved a green building certification in Vietnam. These are concentrated in the industrial sector, initiatives driven by global corporate guidelines, Corporate Social Responsibility (CSR), and the need to reduce operating expenses. However, office buildings and the hospitality sector are also seeing increased green building adoption as property developers seek to attract premium rates and stand out in crowded markets. The residential segment has been lagging on low awareness and short-term cost considerations, though certain technologies such as solar water heaters have taken off.

What drives green initiatives in Vietnam?

Global corporate guidelines are leading many multinationals to go green. This is the case with Big C’s Green Square store in southern Binh Duong province, as well many industrial facilities.

Sales & marketing strategies for offices and residential buildings to enhance brand value, increase occupancy rates, and ultimately attract premium rental fees. President Place, the first LEED gold office building in Vietnam, was opened in 2012 in Ho Chi Minh City, aiming to capitalize on its status as first in market.

Cost savings aimed at reducing operating expenses by building users, especially for energy costs. The need to reduce energy costs will increase in urgency and importance as Vietnam’s government continues to move towards market-based pricing of power, resulting in price hikes.

Low supply of high-grade buildings a chance for green buildings to carve out a niche and attract those companies looking for superior office space to what is currently on the market.

What are the barriers stalling the development of green building?

Low electricity prices relative to the rest of Southeast Asia is a disincentive to promoting energy efficiency. The government is planning to raise electricity prices but tariff hikes have been gradual to limit the impact on inflation, production, and low-income consumers.

Limited skills availability in the market as universities and training institutions are only beginning to address the topic of green buildings.

Short-term thinking and misaligned incentives by property developers focused on short-term costs rather than long-term savings available to building users.

Lack of government incentives has not provided property developers with the short-term benefits needed to drive green building adoption.

Low awareness and price-sensitivity among domestic companies that tend to work with local suppliers without green building materials or technologies, as leading suppliers of green buildings materials and technologies are typically multinational corporations who work primarily with international developers.

Current two primary green certification that is currently used in Vietnam

Property developers in Vietnam have two primary choices when aiming for green building certification: LEED and LOTUS. LEED was developed by the U.S. Green Building Council (USGBC) and is recognized around the world as a leading ratings tool. LOTUS is based on the same principles as other green buildings ratings tools including LEED but it was developed to fit Vietnam’s climate, infrastructure, regulations, and level of economic development in order to increase its relevance to the local market.

At present, there are more LEED-certified buildings in Vietnam but the first pilot set of criteria for LOTUS was only introduced in 2010. With support from VGBC and due to its local relevance, LOTUS will continue to gain in prominence in Vietnam.

Cost and Benefits of Going Green in Vietnam

Short term costs: A primary barrier to green building adoption is short-term cost considerations and the perception that going green is markedly more expensive than not doing so. But is it really that much more expensive to go green? As LOTUS certification has yet to become widely adopted, data on implementation costs are not yet available. However, experience from implementation in other tropical areas shows that the cost premium for going green is anywhere from 1-10% that of a normal building. With local suppliers of green building materials and technologies still limited in Vietnam, the costs might prove higher in the short-term but as demand for such products increases, supply will rise, and costs will drop.

Long term gains: Payback on investment will happen with lower operating costs as well as increased rental income and potentially higher occupancy rates for green office buildings and hotels. Lower operating costs come primarily in the form of lower electricity bills, with efficient air-conditioners, low-energy lights, and energy-efficient glass each providing anywhere from 5-10% energy savings. In addition to hard monetary savings, a greener building that provides natural light, improved air quality and access to green space has been demonstrated to improve employee productivity and lower absentee rates.

Developing a skilled workforce to build green

For the green buildings industry to take off, green building industry leaders with the required skills need to emerge. Developing these skills at Vietnam’s universities will be key to promoting green buildings.

A handful of universities and training centres have responded to the small, but, growing market demand by offering green architecture and energy-saving classes, as well as hosting urban development and energy-saving conferences through partnership with foreign universities.

The private sector is also involved in green initiatives. For example, Holcim promotes green and sustainable practices in Vietnam by holding a competition for universities students annually. The challenge is to develop green and sustainable ideas. The jury votes and Holcim finances the best ideas into reality.

The Vietnam green building Council (VGBC), key to skills development in Vietnam, began offering LOTUS training in June 2011 with its LOTUS Accredited Professional course and Green Buildings Basics. Interest in LOTUS training courses has mainly been concentrated in Ho Chi Minh City, which registers 3x more participants than Hanoi.

How is Vietnam’s regulatory environment impacting green building development?

While economic development has been the primary focus of policymakers, the government has begun to put regulations in place designed to promote energy efficient buildings and define a green buildings development road map. During the period of 2005-2012, a series of laws were passed to promote energy efficiency.

What is needed to further boost the industry is clear and attractive incentives for developers to build green, possibly including preferential and fast-track approvals process for new building permits, as well as the establishment of green building standards in public buildings, which would help raise awareness and drive demand for green building materials and technologies.

How can industry players, Government agencies, civil society, and multilaterals boost the industry in Vietnam?

Industry players can…

• Generate demand by raising awareness, promoting showcase projects, and most importantly, demonstrating return on investment.

• Develop and promote products and technologies that are suitable to Vietnam’s environment and market.

• Partner with other leading multinationals to offer integrated and complementary green buildings solutions.

• Get involved through Vietnam Green Building Council (VGBC), EuroCham’s GreenBiz Working Group, and other industry associations to advise the government on regulatory reform, promote best practices, and build a network of like-minded professionals.

• Support universities and advise them on the development of a green building curriculum, as well as offer internships to students to give them practical, on-the-ground experience in the industry.

Government agencies can…

• Implement incentives for developers to build green

• Establish green building standards for public buildings

• Define a green buildings development road map, following the release of the Green Growth Strategy

• Carrot and stick approach – in addition to offering incentives, provide clear punishments for those violating green buildings regulations and regularly enforce

Vietnam Green Building Council can…

• Train people who work in sustainable construction (architects, project managers, suppliers)

• Develop green buildings network, raise awareness in Vietnam

• Advocate and advise policymakers

Multilateral agencies can…

• Initiate and finance trainings on green buildings and LOTUS through Vietnam’s NGO network

• Offer technical advice to government ministries to improve the regulatory environment

Source: Is There a Future for Green Buildings in Vietnam? (white paper by Solidiance & VGBC)

Link : http://www.solidiance.com/whitepaper/is-there-a-future-for-green-buildings-in-vietnam.pdf

This article was published in Building Review Journal vol 29 no. 1. For more market insights and White Papers, please visit Solidiance.

Landscaping for urban spaces and high rise

Reading Time: 11 minutes

This article was first published in Building Review Journal Vol 29 No. 1 in Jan 2014.

In rural and low density urban areas, greening the built environment is one of the most feasible and cost effective mitigation options. Simple implementations that include a garden and a pond into the building design can be found in many countries. Taking a traditional house setting in Vietnam for example, plants in the garden may provide herbs, vegetables, fruits and flowers, absorb carbon dioxide, offer shade and cool the ambient temperature. The pond collects rainwater run-off, supplies water for garden irrigation, and can be used to grow fish, and create a pleasant microclimate through evaporative cooling.

Building integrated greenery systems allow the provision of greenery beyond the conventional garden and courtyard, to the building itself (such as roof and facade) and even becoming part of a building component (such as a sky terrace). These technologies are relevant in high density urban settings, where land is scarce.

In the technological aspect, the performance of building integrated greenery systems has been improved, thanks to the development of new substrate system, built-in automatic irrigation systems with rain sensors, and built-in drainage systems. Such technologies help to make the greenery systems more lightweight, more water efficient, less maintenance intensive, and to eliminate potential water leakage problems.

The application of green roofs and green facades/walls is also shifting from in-situ application – assembling the green roof layer by layer directly on the roof to modular based. Such application provides shorter installation time, minimum risk of damaging building materials, flexibility in design by mixing and matching various type of plants to create interesting design patterns, and ease of maintenance and replacement.

In green roofs, modules are small trays with sizes ranging from 0.25 to 2m2. Each tray is equipped with drainage, drip irrigation (optional), filter layer, substrate, media layer and grass or shrubs. In green facades or walls, modulisation is applicable for carrier system types. Each carrier panel is a module with a depth ranging from 100mm to 250mm. The modules can be lined up on a metal frame, which is fixed onto facade/wall surface. Irrigation and drainage pipes are interconnected between the modules and hidden within or behind the frame.

Green facade modular system embedded with irrigation and self drainage technologies

Green Roof

Long popular in Europe, green roof infrastructure is gaining popularity in Singapore, Australia and North America in recent years. Green roofs are most suitable for existing buildings in urban areas. This is because their lightweight system and public inaccessibility do not add significant additional dead-loads on existing roofs, and do not pose any security concerns. To be suitable for a green roof, an existing building roof needs to be relatively flat, with access for installation and periodic maintenance.

Each green roof is unique and often designed to achieve multiple objectives and performance results. The current interest in green roofs is coming to the forefront due to their potential to alleviate several environmental problems common to urban areas as follows:

STORM WATER RUNOFF

In urbanised regions, natural areas well adapted to capturing storm water are replaced with impervious surfaces, such as roadways or buildings. Consequently, during major storm events water quickly runs off of these impervious streets and rooftops, burdening storm sewers, treatment plants, and nearby streams and lakes. Compared to traditional roofing materials, green roof systems detain, filter, and slowly release storm water, thus reducing the peak flows and overall volume of runoff.

By installing green roofs, some natural storm water control benefits are regained. If widely implemented, green rooftops have the potential to reduce storm water runoff and nonpoint source pollution problems in urban and suburban environments.

URBAN HEAT ISLAND EFFECT

Most cities are largely constructed of concrete, asphalt, and brick – materials that all absorb and store heat during the day. Conventional roof surfaces also absorb heat and some have been reported to reach temperatures up to 80°C. The re-radiation of this heat from the building structures can cause air temperatures in large cities to be as much as 12-14°C higher than surrounding suburban and rural areas, an effect that is particularly evident at night. This phenomenon is known as the ‘Urban Heat Island’ effect. As a result of the warmer temperatures, air conditioning use rises, putting summertime strains on local electricity distribution grids. Green roofs can help reduce the Urban Heat Island effect, as transpiring plants lower air temperatures, soil and vegetation trap and absorb much less heat than conventional tar or shingle roofs, and retained storm water allows for the benefits of evaporative cooling.

AIR QUALITY

Warmer Urban Heat Island temperatures also exacerbate air pollution, contributing to the formation of smog and ozone. Warm air updrafts from hot surfaces can circulate fine particulates and degrade air quality. These increases in air pollution raise the risk of health complications, and reduce the quality of life for the millions of urban citizens.

Green roofs indirectly help alleviate these air pollution problems. Plants on rooftops could contribute directly to enhanced air quality by trapping and absorbing nitrous oxides, volatile organic compounds, and particulates.

ENERGY CONSERVATION

By providing shading, insulation, and evaporative cooling, green roofs can lower energy use and costs, particularly on the top floor of buildings. Green roofs are most effective where the roof of the structure is flat or slightly pitched, and the roof represents a significant portion of the building surface area. Moreover, rooftop garden plants located near intakes for air conditioning systems will transpire, lowering the temperature of incoming air and reducing costs to cool the building’s air supply. The additional insulation provided by the green roof materials could even cut energy use and costs during winter.

Here are some examples of buildings with green roofs:

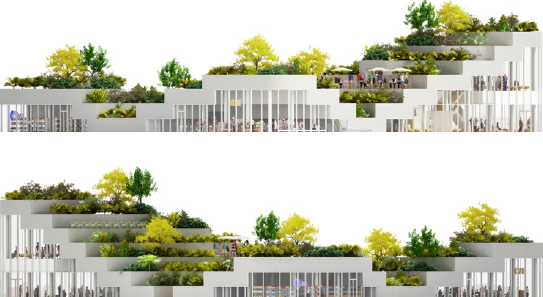

1) School of Art, Design and Media at Nanyang Technological University.

Nanyang Technological University (NTU) is a major research university in Singapore, and the School of Art, Design and Media is Singapore’s first professional art school. The university’s main 200-hectare garden campus, known as the Yunnan Garden campus, is in the south-western part of the island. This 5 story facility sweeps a wooded corner of the campus with an organic, vegetated form that blends landscape and structure, nature and high-tech, and symbolizes the creativity it houses.

The curving green roof distinguish the building from among the other structures on campus but the line between landscape and building is blurred. The roofs serve as informal gathering spaces challenging linear ideas and stirring perception.

The building is oriented with its facades facing north and south to minimize solar gain. Additionally, the green roofs lower both the roof temperature and ambient temperature hence reducing heat gain to the air conditioned building. The rain water collection system is fitted on the green roofs for irrigation. Rain sensors are also installed to automate the irrigation process whereby irrigation is ceased when it rains.

Location : Singapore

Year of Completion : 2008

Owner : Nanyang Technological University

Architect : CPG Consultants Pte Ltd

Photo : Ivan Martha Dinata

2) Punggol Breeze

To realise the vision of Punggol Breeze as a lush and tranquil sanctuary, concerted effort was made to incorporate expansive greenery and integrate them with community spaces for residents. One of the highlights is a 270m linear roof garden atop the multi-storey car park, currently the longest roof garden in Punggol. While the extensive greenery helps to reduce heat and glare, the central location of the roof garden in the precinct enables residents to enjoy the breathtaking sight of verdant foliage from their homes. To facilitate fostering of familial ties, as well as encourage bonding and interaction amongst the community, social and recreational spaces are carved out for facilities such as the children’s playground, fitness corners, and resting shelters for informal gatherings.

Location: Singapore

Year of Completion: 2012

Owner: Housing & Development Board, Singapore

Architect: Surbana International Consultants Pte Ltd

Photos: Housing Development Board, Singapore

3) Super Market at Sanya Lake Park

Most grocery stores in China are large, windowless boxes devoid of light and air, or having their facades covered with advertisements; seemingly only meant for the utilitarian purpose of selling food. NL Architects was tasked to design a super market appropriate for the tropical resort town of Sanya, the southernmost city in China.

Rather than leave the market at ground level – which will take up much of the public space and also expose a potentially unattractive interface to the public, the Dutch firm pushed the grocery store underground, replaced the ground level with retail, and topped it off with a lush, terraced green roof.

The terraced roof is a public space planted with lush vegetation which surrounds benches, paths and tables and chairs for people to sit on and enjoy. Inspired by rice paddies, the roof creates a pleasant atmosphere, a place to relax and a more pleasant view from the surrounding residential buildings.

Location : Sanya, Hainan Province, China

Year of Completion : 2014

Owner : Vanke Real Estate Development Co., Ltd. Hainan

Architect : NL Architects

Photos : NL Architects

Green Facades & Walls

Green walls are at the cutting edge of design and are safe to install on almost any structure, indoors and outdoors. They can make a dramatic statement and create a welcoming environment for people. Green facades/walls allow plants to grow on building facades or wall surfaces through various means – creepers with self clinging roots on wall surfaces, twining plants on mesh or cable support, and carrier panels with pre-grown plants fixed vertically on walls.

Photo: Thinkstock

The implementation of vertical greenery are increasing in popularity as it can provide the following benefits:

Cooling

One of the benefits of interior plants is that they help cool the air around them through the process of evapotranspiration (the movement of water from the soil, through the plant and into the atmosphere). Large interior plants are also very good reducing temperature through shading. Both of these benefits are especially effective in tall buildings where atrium planting is often employed to help with temperature regulation.

Improvements in Indoor Air Quality

Whether indoor or outdoor, a green wall can help improve air quality – by absorbing carbon dioxide and releasing oxygen, at the same time trapping dust and other pollutants – particulate levels (including airborne spores) can be reduced as much as 20% in some situations.

Noise Reduction

Plants can be effective at reducing background noise. Species selection and positioning are crucial to achieve these effects.

Alleviation of Sick Building Syndrome and Improvements in Well-Being

Studies in Europe have shown that health complaints at work and symptoms associated with Sick Building Syndrome (SBS) can be dramatically reduced by the addition of good plant displays.

Office buildings with large floor areas and deep plans (e.g. low and wide buildings) are seldom ‘green’ buildings as they can be difficult to ventilate naturally and there is limited access to natural light and views.

Good interior landscaping can give people access to an indoor garden or views of vegetation, especially if there is an atrium or other large space, and the combination of plants and artificial daylight can help overcome the problems of insufficient natural daylight.

Green Certification

Green Walls contribute directly to achieving credits, or earning credits when used with other sustainable building elements.

Building Structure Protection

Buildings are exposed to the weathering elements and over time, some of the organic construction materials might begin to break down as a result of contraction and expansion. Plants will help to protect the exterior finishes from UV radiation, the elements, and temperature fluctuations that wear down materials.

Here are the examples of buildings with green facade/walls:

1) Rainforest Rhapsody

Named the “Rainforest Rhapsody”, the vertical garden of about 2,000sq ft is populated by a rich array of about 120 plant species.

The vertical garden, installed at the main lobby of Six Battery Road, a Grade A office building, is an iconic attraction and a testament to the Green Mark Platinum award received by the building from the Building & Construction Authority of Singapore.

The design and installation of the vertical garden cost about S$750,000. This is the first vertical garden in Singapore created by Dr Patrick Blanc, in close collaboration with the CapitaLand team. Dr Blanc is an award-winning French botanist and creator of over 140 vertical gardens around the world.

Rainforest Rhapsody is designed with the various plant species arranged and planted in an oblique direction, inspired by the natural growth pattern of plants which grow along the cracks of rocks or any vertical surface. Using a technique pioneered by Dr Blanc, the way the plants are grown in the vertical garden is similar to how plants grow without soil on natural vertical cliff surfaces as well as epiphytically on the branches of rainforest trees throughout the world. Harvested rainwater and nutrients are absorbed by the plants through a controlled irrigation process. The plants absorb environmental pollutants, add oxygen to the air, and also refresh the building’s lobby.

Location : Singapore

Year of Completion : 2011

Owner : CapitaLand

Landscape Design : Patrick Blanc

Photos : Patrick Blanc

2) Bosco Verticale

Bosco Verticale is the World’s first ever vertical forest. Located in Milan, one of the most polluted cities in the world, the Bosco Verticale project aims to mitigate some of the environmental damage that has been inflicted upon the city by urbanization. The design consists of two high-density tower blocks with integrated photovoltaic energy systems, and measure 110 and 76 metres tall respectively. They have the capacity to hold 480 big and medium size trees, 250 small size trees, 11,000 ground-cover plants and 5,000 shrubs (that’s the equivalent of 2.5 acres of forest).

The plants help capture carbon dioxide and dust in the air, reduce the need to mechanically heat and cool the tower’s apartments, and help mitigate the area’s urban heat island effect – particularly during the summer when temperatures can reach over 38 degree celcius. Grey waters produced by the building are filtered and reused for plant irritation. The management and maintenance of the Bosco Verticale’s vegetation is centralised and entrusted to an agency with an office counter open to the public.

Location : Milan, Italy

Owner : Fondo Porta Buova Isola

Architects : Boeri Studio

Year of Completion : 2013

Photos : Boeri Studio

3) One Central Park

Designed by Award-Winning Parisian architect Jean Nouvel, and French artist and botanist Patrick Blanc, One Central Park offered Nouvel and Blanc a canvas of an entirely new scale. They built an integrated experience for living in harmony with the natural world.

The public park at the heart of the precinct climbs the side of the floor-to-ceiling glass towers to form a lush 21st century canopy. Using 250 species of Australian flowers and plants, the buds and blooms of the vegetation form a musical composition on the facade. Vines and leafy foliage spring out between floors and provide the perfect frame for Sydney’s skyline.

Location : Sydney, Australia

Year of Completion : 2013

Owner : Frasers Property

Architect : Jean Nouvel

Photos : Patrick Blanc and Atelier Jean Nouvel

4) Standalone HyGroWall

The HyGroWall, innovated by Vertical Green Pte Ltd, is one of the thinnest vertical garden structures in Singapore.

The stand alone HyGroWall was installed in an office located along Burn Road. Its self standing structure is movable and requires no installation, making it very suitable for small residential units or offices.

The choice of plants are the core of the vertical growth technique, thus shade-loving plants were selected and provided with plant growth lightings in replacement of natural sunlight.

The thin structure is composed of different layers of irrigation geotextile on which the plants will grow on to. This enables a large number of species to grow on the vertical surface, allowing for variety and artistic freedom in the design. The structure includes an irrigation system, providing the plants with a nutrient solution, and the irrigation process occurs for a few minutes each day automatically. As this system is fully automated, the maintenance requirement is minimal. Simple maintenance includes pruning, plant replacement as well as top-up of nutrient supply.

Location : Singapore

Year of Completion : 2013

Landscape Design : Vertical Green Pte Ltd

Photos : Vertical Green Pte Ltd