Asia Pacific (APAC) construction markets are demonstrating resilience in the face of global uncertainty and a broad economic slowdown. According to Linesight’s latest Construction Market Insights report, output is expected to grow steadily through 2025, driven by robust activity in mission-critical sectors such as data centres, infrastructure, high-tech industrial, and energy. However, evolving trade policies and US tariffs may present headwinds. Singapore’s construction industry remains on a healthy growth trajectory, expanding by 3.3 percent in 2024. Construction contracts surged 34 percent year-on-year in the first nine months.

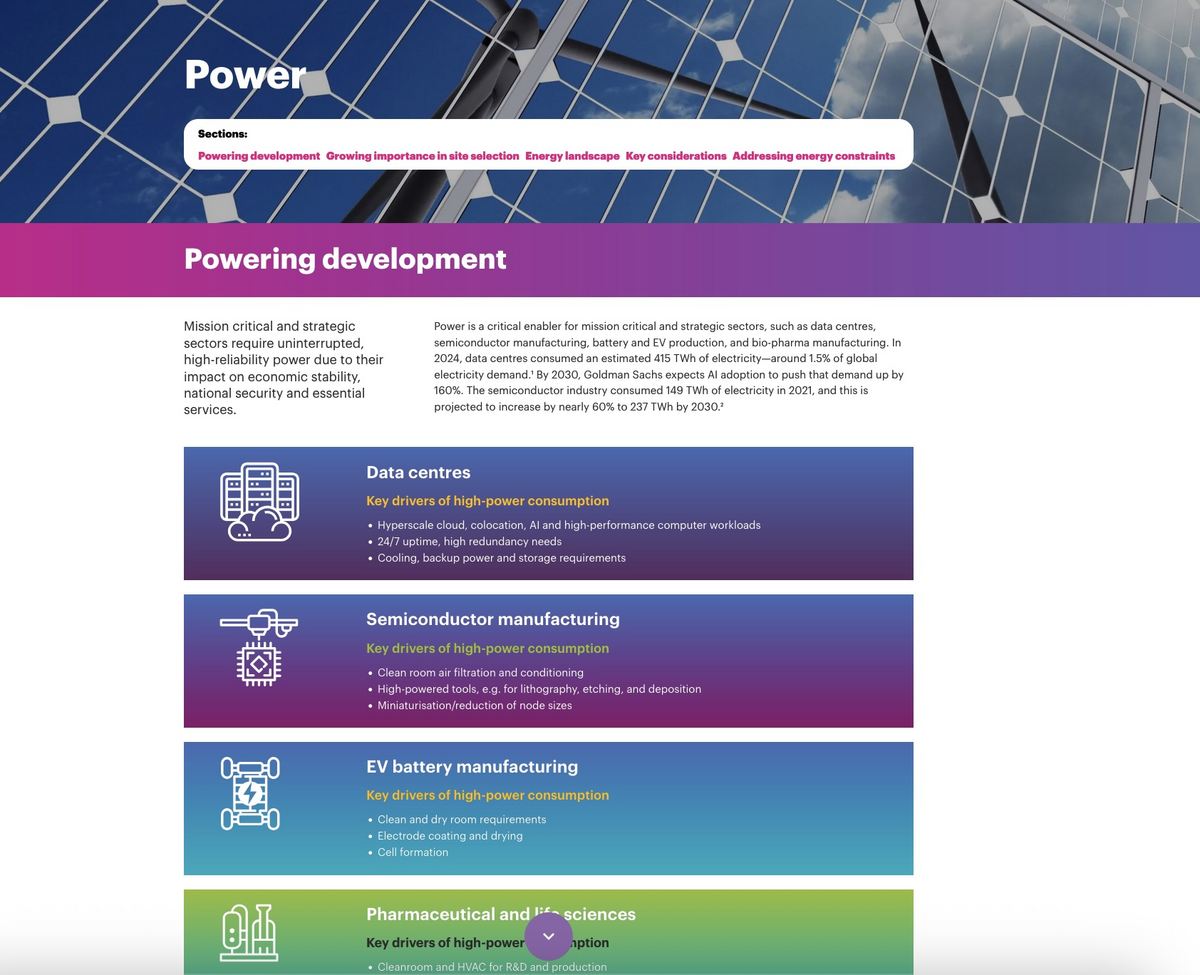

From 2025 to 2028, the sector is projected to grow at an average annual rate of 4.1 percent, driven by investments in oil and gas, transport and renewable energy projects. A new focus in this report is the growing strain on power infrastructure. Power is a critical enabler for mission critical sectors, making uninterrupted and high-reliability power essential given their impact on economic stability, national security and essential services.

As energy-intensive sectors expand, the demand for reliable electricity is becoming a critical challenge. While APAC’s energy supply has grown over the past decade, grid reliability remains inconsistent. Advanced economies like Singapore, Japan, and South Korea enjoy minimal downtime, while emerging markets continue to face reliability gaps.

Despite Asia being home to 83 percent of the world’s coal power, the region is leaning into the shift towards renewable energy and aims to triple renewable capacity by 2030. Significant investments are being made into renewables and grid modernisation, which is expected to help meet the accelerated demand for energy consumption in APAC – a demand that is growing faster than the global average.

Governments are also doubling their efforts to support the critical undertaking of securing clean power, with Singapore most recently topping up its Future Energy Fund and strengthening its capabilities to deploy nuclear power. The report also highlighted key opportunities and considerations from a sectoral perspective, including:

Data Centres

- APAC is experiencing a surge in data centre investment. Seven of the top ten countries by 5G Standalone (SA) reach were in Asia Pacific, with India at 51 percent and Singapore at 37 percent.

- The region is poised to be the fastest-growing region for data centre colocation over the next five years, commanding a massive data centre construction pipeline valued at US$56.4 billion.

- This demand is reshaping energy strategies and countries are turning to renewable energy to support expanding digital infrastructure, meet ESG mandates, incorporate cooling technologies, and importantly, to bolster power reliability.

Life Sciences

- APAC is strengthening its position as a global biopharmaceutical hub and emerging as a key player in mRNA vaccine development.

- The region currently accounts for 16 percent of R&D companies with headquarters in the region. Sustainability remains a priority, with renewable energy and green biomanufacturing playing a key role in reducing GHG emissions and meeting ESG targets.

- Skilled labour shortages and supply chain uncertainty remain as ongoing challenges across the region. With improving infrastructure and supportive policies, APAC is well-positioned to attract pharmaceutical companies looking to diversify their supply chains amid geopolitical tensions.

High-tech industrial

- Investment in the development of semiconductor fabrication plants and proactive policy environments are securing APAC as a dominant high-tech region.

- At the heart of this lies the semiconductor sector, with Taiwan taking a lead as an unparalleled mature market and Singapore following closely as an established market that hosts a full-spectrum of the semiconductor ecosystem.

- Given the resource-intensive nature of semiconductor manufacturing, challenges around power reliability and grid capacity will need to be mitigated.

In 2024, the construction sector saw commodity price corrections. However, new tariffs may disrupt global supply chains in the near term. In Singapore, prices for key materials like copper, steel rebar, and cement have declined due to global trade uncertainties. Notably, steel rebar prices are forecasted to drop 13 percent year-on-year in Q2 2025, driven by oversupply and competitive exports from China.

Scott Halyday, Regional Director, Southeast Asia at Linesight, said, “While near-term economic outlook has been clouded by rising trade tensions, we remain cautiously optimistic that APAC is set to show resilient growth in its construction markets with a strong pipeline of planned projects. In an environment of heightened risk and volatility, risk management and robust scenario planning will be crucial for developers and businesses to pre-empt and cushion impacts.”