The Urban Land Institute (ULI) has boosted its research and thought leadership capabilities across Asia Pacific with the appointment of Mark Cooper as Senior Director, Thought Leadership of ULI Asia Pacific.

Mark has more than 25 years of experience as a real estate journalist, with 15 years covering the Asia Pacific region. He was formerly editor of industry magazines: AsiaProperty, EuroProperty and IPE Real Estate. Before joining ULI in Hong Kong, he was a freelance writer, researcher and consultant. Mark will produce research and thought leadership content in a variety of formats, focusing on ULI’s core themes and global mission priorities around; sustainability and decarbonisation, housing attainability, capital markets and technology and innovation.

On sustainability and decarbonisation, Mark will work with Jenny Zhang, Director of Sustainability, ULI Asia Pacific. Jenny leads programmes around decarbonisation across the Asia Pacific region, notably the recent Low Carbon Emissions Steel Initiative in China’s real estate sector. Jenny will be supported by Vidyashree Unnikrishnan, who also joined ULI in January as Senior Researcher and is based in Bangalore. Vidyashree has a Master’s degree in Environmental Building Design from the University of Pennsylvania and was formerly ESG Manager for Grosvenor for two years.

May Chow, Chief Development Officer of ULI Asia Pacific, adds, “ULI is a member-centric organisation and we are passionate about collaborating as a powerful collective to deliver industry impact as well as a significant membership value proposition. Our Thought Leadership team will build on our convening platform of regional events, including workshops and conferences, by highlighting key insights drawn from the expertise in the room and developing these in greater depth for wider distribution.”

Alan Beebe, Chief Executive of ULI Asia Pacific, said: “Our members comprise professionals from across the real estate value chain and they are a hugely valuable source of industry expertise. Expanding our thought leadership capabilities in-house, allows us to channel much of this extensive knowledge, and firmly position ULI as an industry thought leader across Capital Markets, Housing Attainability and the Decarbonisation of the Built Environment. Mark is already a well-established industry ‘thought leader’ and we are delighted to have him on board to spearhead this regional initiative. Additionally, I would like to personally thank our philanthropic donors and corporate sponsors who have helped us to realise our vision, and we look to continue partnering with industry organisations to further support our mission priorities in Asia Pacific.”

Mark Cooper said: “I am delighted to join ULI and look forward to building on the success of market-leading reports such as Emerging Trends in Real Estate Asia Pacific and the Home Attainability Index. We plan to develop a broad range of thoughtful and useful content, which will help members and the wider industry navigate an increasingly complex real estate landscape.”

https://brj.com.sg/wp-content/uploads/2025/02/image1-16.png6271200Editorial StaffEditorial Staff2025-02-27 11:00:002025-02-25 15:10:19ULI Expands Thought Leadership Team in Asia Pacific

The Urban Land Institute (ULI) in Asia Pacific has hired Terri Seow to take on the role of Executive Director for Singapore, a Council with over 600 members. Seow was formerly at BBC Global News for over 16 years, where she was Vice President, Marketing & Insights, Asia Pacific. In addition to a plethora of regional marketing experience, she joins ULI, the world’s oldest and largest network of experts across the built environment, with a huge passion for environmental sustainability.

Seow was also formerly the Going Green lead at the BBC, where she was responsible for raising awareness of environmental sustainability for over two years. During her free time, she is an Adjunct Lecturer for Sustainability Marketing at the National University of Singapore. Her move to ULI continues the trajectory of working for purpose-led organisations.

Wenshi Zheng, Group Chief Strategy & Sustainability Officer, Frasers Property, commented, “We are glad to welcome Terri as the new Executive Director of ULI Singapore. With deep experience in brand building, marketing, and communications, Terri brings exceptional expertise and vision to our mission. Her passion for sustainability aligns well with ULI’s mission and makes her an outstanding choice to lead ULI Singapore. We are confident that under her leadership, ULI Singapore will continue to thrive and engage our like-minded members to advance ULI’s mission to create resilient, inclusive and sustainable communities.”

Terri Seow, Executive Director, ULI Singapore, adds, “I’m extremely proud to be leading the Singapore chapter of ULI – an organisation that has long been at the forefront of driving positive change in both the environment and communities globally. As someone deeply passionate about creating purpose-led work and advancing a sustainable world, I am thrilled to contribute and do my part in shaping the future of the built environment – an area that has such a profound influence on the world at large. I look forward to working closely with like-minded leaders from the industry to drive meaningful change.”

https://brj.com.sg/wp-content/uploads/2025/01/image1.png8001200developerdeveloper2025-01-20 13:09:492025-01-20 13:09:49ULI Appoints Executive Director in Singapore

The 2024 Asia Pacific Home Attainability Index by the Urban Land Institute (ULI) offers a comprehensive overview of housing attainability across the Asia Pacific region. In this third edition, the report includes data from three additional cities – Bangkok, Kuala Lumpur, and Perth, expanding its coverage to 48 cities in 11 countries, namely, Australia, China (including Hong Kong SAR), India, Indonesia, Japan, Malaysia, Singapore, South Korea, the Philippines, Thailand, and Vietnam.

Alan Beebe, CEO, ULI Asia Pacific, said: “In addition to measuring home attainability for both home ownership and rentals in relation to median household income across 48 cities, the report has also identified key trends and factors affecting home attainability in Asia Pacific region, which represents 60 percent of the world with a population of 4.3 billion people. By identifying key factors impacting housing supply and demand, we can work towards advancing best practices in residential development and to support ULI members and local communities in creating more equitable housing opportunities for all, aligned with our goal at the ULI Asia Pacific Centre for Housing.”

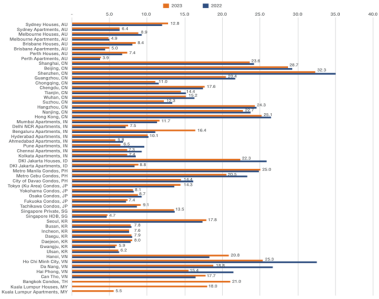

Figure 1: Median/average home price to median annual household income

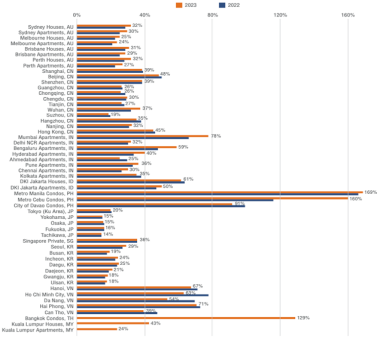

Figure 2: Median/average monthly rent to median monthly household income

2024 ULI Asia Pacific Home Attainability Index Key Trends:

1) In cities experiencing significant immigration inflows, home prices and rent have risen materially.

Popular gateway cities for overseas immigration and studies, such as Singapore, Sydney, and Tokyo, have recorded steep hikes in home prices due to a large influx of immigrants, while key Australian cities including Sydney and Melbourne saw increases in rental rates due to falling vacancy rates of 0.9 percent and 2.2 percent, respectively.

Tokyo’s urban core area consisting of 23 wards has seen its new condominium prices rise by nearly 40 percent, caused by an increase in foreign buyers, primarily from mainland China and the relatively inexpensive prices for a global gateway city. For comparison, even after the price increase, the median price of a new condominium in Tokyo is US$800,000, considerably lower than the median price of over US$1 million for new units in similar urban cores of Tier 1 cities in China such as Shenzhen, Shanghai, and Beijing.

As a result, Tokyo has emerged as an attractive choice for mainland Chinese looking to buy a property outside of China. To curb private home prices, Singapore introduced a 60 percent stamp duty on foreign buyers of private homes, contributing to a 20 percent drop in total home sales.

2) High home prices and rent levels have negatively impacted home attainability for young people in their 20s and 30s. To alleviate the housing shortage and improve home attainability, some national governments are promoting for-rent developments.

At the current price levels, young people in their twenties and thirties living in leading economic centres, especially first-generation young migrants, have little hope of being able to afford a home. This is unless they come from generational wealth or belong to a small minority of otherwise wealthy individuals.

As an example, Bangkok’s median condo price of around US$224,000 is 21 times the median annual household income, while the median monthly rent of US$1,150 represents 129 percent of the median monthly income. In Bengaluru, the return of IT professionals into India’s IT hub following the end of COVID-19 drove the ratio of median home price to median annual household income to 16.4 from 11.1 in the previous year.

To alleviate the housing shortage and improve home attainability, countries and investors are pivoting towards promoting for-rent projects to increase the supply of affordable homes. Australia’s new Labour Party government adopted a housing policy that includes an AU$10 billion (approx. US$6.5 billion) Housing Australia Fund to fund 30,000 new social and affordable rental homes in five years, as well as tax incentives for the development of build-to-rent homes in the private market.

In Singapore, where housing policy is centred on home ownership, the government has recently sold a plot of land with a requirement for large-scale, long-term rental units. This unusual move was made after the Urban Redevelopment Authority (URA) determined that there is sufficient demand for long-term rental housing, especially among young professionals, students, and families in transition, following consultations with the industry.

3) Home buyers and renters are forced to take on financial risks, such as loss of deposits or not receiving their completed homes on time, as home builders and landlords get into financial distress which impacts project completions.

In mainland China, sluggish sales and escalating costs in the past two years have caused many leading home developers to incur unprecedented losses and default on loans. Given that pre-sale of homes before construction is customary in mainland China, buyers of such homes still under construction are placed in a precarious position where they run the risk of not receiving their completed homes on time.

In Australia, in the past two years, over 2,000 home builders went out of business largely due to rising interest rates, building materials and labour costs. Homeowners face substantial financial risks such as not being able to recover deposits or not having the home constructed as agreed.

In Vietnam, many developments have come to a standstill as developers failed to meet interest payments, a situation further exacerbated by the credit crunch spurred by declining bond issuance and a general market turmoil that impacted developers’ liquidity. While the Vietnamese government has implemented countermeasures such as reducing mortgage rates, a new Land Law that emphasises market-driven land valuation could significantly increase the costs of acquiring projects.

Beebe added: “The housing market has been significantly affected by heightened interest rates and rising costs. Homeownership represents the most valuable asset for most households, and the housing sector is a key part of the overall economy. Moving forward, we expect to see governments in the region introduce more countermeasures to rein in rising home prices.”

Other key findings and metrics from the report include:

In terms of home ownership, public housing in Singapore continues to be the most attainable, while homes in Shenzhen are the least attainable. The median price of Housing Development Board (HDB) units, representing 90 percent of the total housing stock in the city-state, is less than 5 times that of the median annual household income, while Shenzhen has the highest ratio of median home prices relative to median annual household income at 32 times, followed by Beijing at 28, and Metro Manila, Ho Chi Minh City, and Hong Kong SAR at around 25.

As for home rental, cities in Japan and South Korea, excluding capitals Tokyo and Seoul, are the most affordable with the lowest ratio of monthly rent to income. Rent in South Korean cities (outside of Seoul) ranges from 18 percent to 25 percent of monthly income, while rent in Japanese cities (outside of Tokyo) ranges from 14 percent to 16 percent of the median monthly household income. Conversely, rent in cities in the Philippines are least affordable, with median monthly rent to median monthly household income near or above 100 percent.

Among the region’s gateway cities, Hong Kong SAR has the lowest home attainability with a median home price of over $1.1 million, which is 25 times the median household income, in contrast to Tokyo and Seoul with home price-to-income ratios of around 15.

It is estimated that Jakarta, Indonesia needs 800,000 additional homes to accommodate new migrants moving to the capital of the world’s fourth most populous country. Of the 2.8 million existing homes, 63 percent are deemed substandard with many without access to the public water system.

Leading cities in developing countries such as India, the Philippines, and Vietnam have been heavily investing in mass transportation infrastructure like new metro lines, which is expected to increase mobility and connectivity between suburbs to city centres. This will expand the area for daily commutes and create opportunities for high-density development projects around stations to increase housing stock.

In this report, home attainability is measured by (i) median home price to median annual household income, ideally less than five times, and (ii) median monthly rent to median monthly household income, ideally less than 30 percent.

A complete list of the 10 key trends and insights are identified by the 2024 Asia Pacific Home Attainability Index. Analyses of home attainability by country are also available in the full report, which can be found on ULI’s Knowledge Finder platform.

https://brj.com.sg/wp-content/uploads/2024/07/image1-4.png8001200developerdeveloper2024-07-10 11:00:342024-07-11 12:10:05ULI Releases 2024 Asia Pacific Home Attainability Index Across 48 Cities