The Urban Land Institute (ULI) has boosted its research and thought leadership capabilities across Asia Pacific with the appointment of Mark Cooper as Senior Director, Thought Leadership of ULI Asia Pacific.

Mark has more than 25 years of experience as a real estate journalist, with 15 years covering the Asia Pacific region. He was formerly editor of industry magazines: AsiaProperty, EuroProperty and IPE Real Estate. Before joining ULI in Hong Kong, he was a freelance writer, researcher and consultant. Mark will produce research and thought leadership content in a variety of formats, focusing on ULI’s core themes and global mission priorities around; sustainability and decarbonisation, housing attainability, capital markets and technology and innovation.

On sustainability and decarbonisation, Mark will work with Jenny Zhang, Director of Sustainability, ULI Asia Pacific. Jenny leads programmes around decarbonisation across the Asia Pacific region, notably the recent Low Carbon Emissions Steel Initiative in China’s real estate sector. Jenny will be supported by Vidyashree Unnikrishnan, who also joined ULI in January as Senior Researcher and is based in Bangalore. Vidyashree has a Master’s degree in Environmental Building Design from the University of Pennsylvania and was formerly ESG Manager for Grosvenor for two years.

May Chow, Chief Development Officer of ULI Asia Pacific, adds, “ULI is a member-centric organisation and we are passionate about collaborating as a powerful collective to deliver industry impact as well as a significant membership value proposition. Our Thought Leadership team will build on our convening platform of regional events, including workshops and conferences, by highlighting key insights drawn from the expertise in the room and developing these in greater depth for wider distribution.”

Alan Beebe, Chief Executive of ULI Asia Pacific, said: “Our members comprise professionals from across the real estate value chain and they are a hugely valuable source of industry expertise. Expanding our thought leadership capabilities in-house, allows us to channel much of this extensive knowledge, and firmly position ULI as an industry thought leader across Capital Markets, Housing Attainability and the Decarbonisation of the Built Environment. Mark is already a well-established industry ‘thought leader’ and we are delighted to have him on board to spearhead this regional initiative. Additionally, I would like to personally thank our philanthropic donors and corporate sponsors who have helped us to realise our vision, and we look to continue partnering with industry organisations to further support our mission priorities in Asia Pacific.”

Mark Cooper said: “I am delighted to join ULI and look forward to building on the success of market-leading reports such as Emerging Trends in Real Estate Asia Pacific and the Home Attainability Index. We plan to develop a broad range of thoughtful and useful content, which will help members and the wider industry navigate an increasingly complex real estate landscape.”

https://brj.com.sg/wp-content/uploads/2025/02/image1-16.png6271200Editorial StaffEditorial Staff2025-02-27 11:00:002025-02-25 15:10:19ULI Expands Thought Leadership Team in Asia Pacific

The Urban Land Institute (ULI) in Asia Pacific has hired Terri Seow to take on the role of Executive Director for Singapore, a Council with over 600 members. Seow was formerly at BBC Global News for over 16 years, where she was Vice President, Marketing & Insights, Asia Pacific. In addition to a plethora of regional marketing experience, she joins ULI, the world’s oldest and largest network of experts across the built environment, with a huge passion for environmental sustainability.

Seow was also formerly the Going Green lead at the BBC, where she was responsible for raising awareness of environmental sustainability for over two years. During her free time, she is an Adjunct Lecturer for Sustainability Marketing at the National University of Singapore. Her move to ULI continues the trajectory of working for purpose-led organisations.

Wenshi Zheng, Group Chief Strategy & Sustainability Officer, Frasers Property, commented, “We are glad to welcome Terri as the new Executive Director of ULI Singapore. With deep experience in brand building, marketing, and communications, Terri brings exceptional expertise and vision to our mission. Her passion for sustainability aligns well with ULI’s mission and makes her an outstanding choice to lead ULI Singapore. We are confident that under her leadership, ULI Singapore will continue to thrive and engage our like-minded members to advance ULI’s mission to create resilient, inclusive and sustainable communities.”

Terri Seow, Executive Director, ULI Singapore, adds, “I’m extremely proud to be leading the Singapore chapter of ULI – an organisation that has long been at the forefront of driving positive change in both the environment and communities globally. As someone deeply passionate about creating purpose-led work and advancing a sustainable world, I am thrilled to contribute and do my part in shaping the future of the built environment – an area that has such a profound influence on the world at large. I look forward to working closely with like-minded leaders from the industry to drive meaningful change.”

https://brj.com.sg/wp-content/uploads/2025/01/image1.png8001200developerdeveloper2025-01-20 13:09:492025-01-20 13:09:49ULI Appoints Executive Director in Singapore

The 2024 Asia Pacific Home Attainability Index by the Urban Land Institute (ULI) offers a comprehensive overview of housing attainability across the Asia Pacific region. In this third edition, the report includes data from three additional cities – Bangkok, Kuala Lumpur, and Perth, expanding its coverage to 48 cities in 11 countries, namely, Australia, China (including Hong Kong SAR), India, Indonesia, Japan, Malaysia, Singapore, South Korea, the Philippines, Thailand, and Vietnam.

Alan Beebe, CEO, ULI Asia Pacific, said: “In addition to measuring home attainability for both home ownership and rentals in relation to median household income across 48 cities, the report has also identified key trends and factors affecting home attainability in Asia Pacific region, which represents 60 percent of the world with a population of 4.3 billion people. By identifying key factors impacting housing supply and demand, we can work towards advancing best practices in residential development and to support ULI members and local communities in creating more equitable housing opportunities for all, aligned with our goal at the ULI Asia Pacific Centre for Housing.”

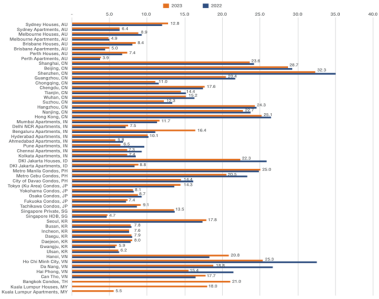

Figure 1: Median/average home price to median annual household income

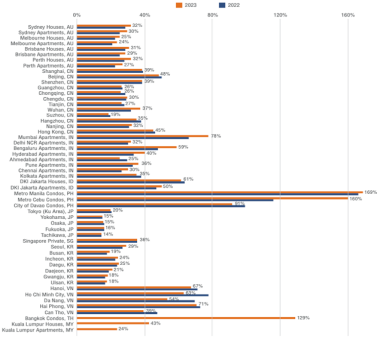

Figure 2: Median/average monthly rent to median monthly household income

2024 ULI Asia Pacific Home Attainability Index Key Trends:

1) In cities experiencing significant immigration inflows, home prices and rent have risen materially.

Popular gateway cities for overseas immigration and studies, such as Singapore, Sydney, and Tokyo, have recorded steep hikes in home prices due to a large influx of immigrants, while key Australian cities including Sydney and Melbourne saw increases in rental rates due to falling vacancy rates of 0.9 percent and 2.2 percent, respectively.

Tokyo’s urban core area consisting of 23 wards has seen its new condominium prices rise by nearly 40 percent, caused by an increase in foreign buyers, primarily from mainland China and the relatively inexpensive prices for a global gateway city. For comparison, even after the price increase, the median price of a new condominium in Tokyo is US$800,000, considerably lower than the median price of over US$1 million for new units in similar urban cores of Tier 1 cities in China such as Shenzhen, Shanghai, and Beijing.

As a result, Tokyo has emerged as an attractive choice for mainland Chinese looking to buy a property outside of China. To curb private home prices, Singapore introduced a 60 percent stamp duty on foreign buyers of private homes, contributing to a 20 percent drop in total home sales.

2) High home prices and rent levels have negatively impacted home attainability for young people in their 20s and 30s. To alleviate the housing shortage and improve home attainability, some national governments are promoting for-rent developments.

At the current price levels, young people in their twenties and thirties living in leading economic centres, especially first-generation young migrants, have little hope of being able to afford a home. This is unless they come from generational wealth or belong to a small minority of otherwise wealthy individuals.

As an example, Bangkok’s median condo price of around US$224,000 is 21 times the median annual household income, while the median monthly rent of US$1,150 represents 129 percent of the median monthly income. In Bengaluru, the return of IT professionals into India’s IT hub following the end of COVID-19 drove the ratio of median home price to median annual household income to 16.4 from 11.1 in the previous year.

To alleviate the housing shortage and improve home attainability, countries and investors are pivoting towards promoting for-rent projects to increase the supply of affordable homes. Australia’s new Labour Party government adopted a housing policy that includes an AU$10 billion (approx. US$6.5 billion) Housing Australia Fund to fund 30,000 new social and affordable rental homes in five years, as well as tax incentives for the development of build-to-rent homes in the private market.

In Singapore, where housing policy is centred on home ownership, the government has recently sold a plot of land with a requirement for large-scale, long-term rental units. This unusual move was made after the Urban Redevelopment Authority (URA) determined that there is sufficient demand for long-term rental housing, especially among young professionals, students, and families in transition, following consultations with the industry.

3) Home buyers and renters are forced to take on financial risks, such as loss of deposits or not receiving their completed homes on time, as home builders and landlords get into financial distress which impacts project completions.

In mainland China, sluggish sales and escalating costs in the past two years have caused many leading home developers to incur unprecedented losses and default on loans. Given that pre-sale of homes before construction is customary in mainland China, buyers of such homes still under construction are placed in a precarious position where they run the risk of not receiving their completed homes on time.

In Australia, in the past two years, over 2,000 home builders went out of business largely due to rising interest rates, building materials and labour costs. Homeowners face substantial financial risks such as not being able to recover deposits or not having the home constructed as agreed.

In Vietnam, many developments have come to a standstill as developers failed to meet interest payments, a situation further exacerbated by the credit crunch spurred by declining bond issuance and a general market turmoil that impacted developers’ liquidity. While the Vietnamese government has implemented countermeasures such as reducing mortgage rates, a new Land Law that emphasises market-driven land valuation could significantly increase the costs of acquiring projects.

Beebe added: “The housing market has been significantly affected by heightened interest rates and rising costs. Homeownership represents the most valuable asset for most households, and the housing sector is a key part of the overall economy. Moving forward, we expect to see governments in the region introduce more countermeasures to rein in rising home prices.”

Other key findings and metrics from the report include:

In terms of home ownership, public housing in Singapore continues to be the most attainable, while homes in Shenzhen are the least attainable. The median price of Housing Development Board (HDB) units, representing 90 percent of the total housing stock in the city-state, is less than 5 times that of the median annual household income, while Shenzhen has the highest ratio of median home prices relative to median annual household income at 32 times, followed by Beijing at 28, and Metro Manila, Ho Chi Minh City, and Hong Kong SAR at around 25.

As for home rental, cities in Japan and South Korea, excluding capitals Tokyo and Seoul, are the most affordable with the lowest ratio of monthly rent to income. Rent in South Korean cities (outside of Seoul) ranges from 18 percent to 25 percent of monthly income, while rent in Japanese cities (outside of Tokyo) ranges from 14 percent to 16 percent of the median monthly household income. Conversely, rent in cities in the Philippines are least affordable, with median monthly rent to median monthly household income near or above 100 percent.

Among the region’s gateway cities, Hong Kong SAR has the lowest home attainability with a median home price of over $1.1 million, which is 25 times the median household income, in contrast to Tokyo and Seoul with home price-to-income ratios of around 15.

It is estimated that Jakarta, Indonesia needs 800,000 additional homes to accommodate new migrants moving to the capital of the world’s fourth most populous country. Of the 2.8 million existing homes, 63 percent are deemed substandard with many without access to the public water system.

Leading cities in developing countries such as India, the Philippines, and Vietnam have been heavily investing in mass transportation infrastructure like new metro lines, which is expected to increase mobility and connectivity between suburbs to city centres. This will expand the area for daily commutes and create opportunities for high-density development projects around stations to increase housing stock.

In this report, home attainability is measured by (i) median home price to median annual household income, ideally less than five times, and (ii) median monthly rent to median monthly household income, ideally less than 30 percent.

A complete list of the 10 key trends and insights are identified by the 2024 Asia Pacific Home Attainability Index. Analyses of home attainability by country are also available in the full report, which can be found on ULI’s Knowledge Finder platform.

https://brj.com.sg/wp-content/uploads/2024/07/image1-4.png8001200developerdeveloper2024-07-10 11:00:342024-07-11 12:10:05ULI Releases 2024 Asia Pacific Home Attainability Index Across 48 Cities

In a market accustomed to abundant supplies of cheap debt, the real estate landscape in Asia Pacific (APAC) is undergoing a significant transformation following the series of rapid interest rate hikes initiated by the US Federal Reserve since mid-2022, according to the 18th edition of the Emerging Trends in Real Estate® Asia Pacific 2024 Report, the regional real estate forecast jointly published by the Urban Land Institute (ULI) and PwC. The report is based on a survey of 149 real estate professionals and 54 interviews with investors, developers, property company representatives, and lender brokers.

In the absence of asset revaluations, far fewer deals are now able to deliver accretive returns, prompting large global investors to retreat to the sidelines as they wait for markets to reset. Traditional asset classes often pursued by global investors – large, core, office and retail assets – have also fallen from favour as yields have not yet expanded to match the expectations of potential buyers, resulting in a bid-ask standoff.

As they seek out assets that offer yields able to match revised underwriting thresholds, investors are pivoting to alternative asset classes, including those in the “beds” category, such as multifamily residential projects, student housing, senior living, and hotels, as travel and tourism continue their rebound. Other alternative asset classes include logistics, data centres, and life science assets. Alternatives are popular due to their potential to tap tailwinds of demand generated by technological, demographic, or social trends that are uncorrelated with macroeconomic fluctuations.

The higher interest rate environment affects not just the financing of new deals, but also the refinancing of purchased assets, creating the prospect of a “refinancing wall” that may drive a wave of selling by owners unable or unwilling to recapitalise. The tightened traditional bank lending has catalysed a financing gap of as much as US$5.8 billion for private credit to fill.

The report highlights how transition risk arising from energy efficiency issues has become a critical factor impacting asset valuations. Properties failing to meet environmental standards may face market discounts, emphasising the growing importance of aligning real estate portfolios with sustainable practices.

Alan Beebe, CEO, ULI Asia Pacific said, “As investors are re-evaluating their strategies, a ripple effect on real estate markets is widespread. There is an urgency for real estate to align with environmental standards, and adaptation and informed decision-making will be key to manoeuvring this new chapter in real estate financing.”

Stuart Porter, PwC Asia Pacific Real Estate Tax Leader said, “Amidst this transformative phase in APAC’s real estate landscape, investors are at a juncture where strategic alignment with sustainable practices for resilient real estate portfolios will be critical. The shift towards alternative asset classes signifies an evolving investment model fuelled by diverse socio-economic trends.”

Against a backdrop of sharply reduced overall investment, the share referable to regional cross-border flows has held up well (i.e., flat, year-on-year in the third quarter of 2023) compared to plunging transactions from global funds (down 64 percent for the same period). One reason for the relative strength of intra-Asian flows – in particular those from Singapore – has been the resilience of regional economies. Another reason has been an upswing in outgoing capital from Japan in search of higher returns.

This year’s top Emerging Trends investment prospect rankings reveal a notably optimistic perspective despite a gloomy global outlook, indicating overall confidence in APAC as a safe haven compared to the West. Unsurprisingly, given that interest rates remain at ultra-low levels, Tokyo and Osaka rank first and third respectively. They are followed by Sydney and Melbourne in second and fifth, reflecting a historical preference for Australian core assets among global investors, together with expectations of strong demand for Grade-A assets. Singapore is ranked fourth place, as investors continue to regard it as a viable core market given the limited supply, ongoing demand for space, and good prospects for rental growth.

Building Review Journal spoke with Ron Pressman, the Global CEO of the Urban Land Institute (ULI), a global organisation focused on promoting responsible land use and sustainable communities.

As the world becomes more aware of the urgent need to address climate change, many industries are taking steps to become more sustainable. Real estate, which accounts for a significant portion of global greenhouse gas emissions, is no exception. But what does it mean for the real estate industry to be sustainable? And how can developers, investors, and policymakers work together to pave a more sustainable way forward? In this interview, Pressman shares his insights on the challenges and opportunities facing the real estate industry, the role of technology and policy in promoting sustainability, and the importance of engaging with local communities in sustainable development.

1. What do you see as the biggest challenges and opportunities for the real estate industry in terms of sustainability?

Real estate represents around 40 percent of the annual carbon emissions. While very fragmented across trillions of square feet of global real estate, it represents the largest segment of addressable carbon emission reduction opportunities. So, it is important to galvanise focus on this. Two big reduction opportunities are running buildings more efficiently and building new projects more sustainably. Roughly two-thirds of the annual global emission footprint arise from operating existing buildings. There are many ways to reduce this via updated heating, cooling, and building management technology. New build embodied carbon from construction, materials, and transportation represents the other “third”. There are many new options to build to a more efficient standard embracing sustainable construction and materials leadership practices.

One of the biggest sustainability challenges for the real estate industry is navigating the regulatory and reporting environment, and then ensuring that the organisational metrics will result in accurate measurement against these regulations and standards. Transparency on sustainability is no longer optional – stakeholders across the industry expect the real estate sector to clearly report on their sustainability performance and progress against goals. The industry is dealing with an alphabet soup of climate regulations and policies that overlap, compete and differ by country and region. There is a lack of consistency globally, and waiting for one is not an option. Therefore, the sector must work together to successfully navigate the road ahead. Collaboration and a balance between ‘quality’ and ‘quantity’ should be the focus.

On the other hand, as the industry pivots to mitigating climate change risks, there are opportunities to bring competitive, cutting-edge buildings to the market. New projects now have ESG regulations and standards embedded by default, and legacy buildings are also being retrofitted to be up to date with the same standards amid the global push for greener buildings. Real estate owners and developers who are proactively incorporating sustainability opportunities into their assets are benefitting from the competitive advantage of green premiums like high-performance buildings, higher quality tenants, lower tenant turnover, and increased asset value.

2. How can real estate developers and investors incorporate sustainability into their decision-making processes?

Conducting a sustainability assessment is one of the ways sustainability can be incorporated in decision-making processes. This includes incorporating sustainability considerations into decisions regarding due diligence, property condition assessments, financing, building operations, and disposition.

Before investing in a property or beginning a development project, it’s essential to conduct a sustainability assessment. This involves evaluating the environmental impact (and associated investment needs) of the project, including factors such as energy consumption, water usage, waste generation, and carbon emissions.

Specifically, the investors should actively understand climate change adaptation needs for key markets. This requires investors to shift from an asset-centric view to a market-level appraisal of risk and resilience drivers. They should consider ways to leverage technical expertise to build the capacity of communities to absorb climate shocks and stressors. Building resilience against the impacts of climate change will require a cooperative ecosystem made up of public, private, non-profit, and academic institutions. To these ends, investors can support the creation of robust community resilience and recovery plans and should direct their investment to infrastructure and real estate asset classes that are climate responsive, adaptable to changing environmental conditions, and enhance the overall social and ecological resilience of communities.

A fundamental problem recognised in Europe is the failure of valuation processes to take account of climate transition risks. High values in an area of high demand can mask the potential for environmental underperformance to lead to an asset stranding while low values in secondary areas undermine the business case for retrofit. Values that reflected transition risk would help to embed sustainability in decision-making.

3. What role can technology play in creating more sustainable buildings and communities?

Aligning sustainability with innovation strategies is one of the key priorities for real estate companies in Asia Pacific, with ESG considered a significant factor in the decision-making for new technologies. PropTech solutions, and more recently ClimateTech solutions, offer tremendous opportunities to advance building decarbonisation and resilience.

By incorporating technology into their operations, building owners and developers can optimise energy usage, reduce greenhouse gas emissions, improve occupant health, bolster resilience against physical climate hazards, and improve the overall sustainability of their buildings and communities.

For example, building automation systems (BAS) can optimise the use of energy and the emission of carbon by automating various functions, including heating, cooling, and lighting, turning them on only when someone is in the room, or shifting some of the building’s energy load to times when the utility grid is cleaner.

4. How can urban planning and policy support more sustainable real estate development?

Urban planning and policy can play a critical role in supporting more sustainable real estate development:

Zoning regulations can enforce more sustainable development patterns, such as mixed-use development, transit-oriented development, and walkable neighbourhoods. Zoning regulations can also require the inclusion of green space, sustainable building materials, and energy-efficient features in new development projects.

Transportation planning can promote sustainable options such as public transit, bike lanes, and pedestrian-friendly streets. This can reduce greenhouse gas emissions and improve air quality by going car-lite or even car-free.

Community engagement is also a crucial element of sustainable urban planning and policy. Engaging with the public in the development process can ensure that the project meets the needs of the local community, respects their values and culture, and helps to create more liveable and sustainable neighbourhoods. It can also help to build support for sustainable development projects, which is essential for their success.

5. What are some examples of innovative and sustainable real estate projects that you have seen around the world?

One of the winners of the 2022 ULI Asia Pacific Awards for Excellence – Wesley Place (pictured above) – is a commercial office project on a 1.1-hectare site near Melbourne city centre, featuring a high degree of sustainability technology, including a thermally efficient façade, smart metering, rooftop solar, waste monitoring and recycling.

However, the project was designed with the S (social) in ESG in mind as well. The office building is complemented by a 5,000-square-metre, nicely scaled, landscaped plaza on the ground floor. The plaza retains 150-year-old trees and has 24-hour public access connecting to a variety of other buildings and amenities.

In addition, the project site incorporates a collection of five significant heritage buildings dating to 1837, including Wesley Church together with its associated Manse. Following long negotiations with Church authorities, the buildings and surrounding spaces have been extensively refurbished, with close attention to details such as restoring stained glass windows and sourcing appropriate masonry from as far away as Europe. The church has remained a place of worship, while the other buildings have been adapted to various commercial purposes, including a café/restaurant in the Manse building that has been integrated into the office-building lobby, creating a unique experience for occupants.

The exercise was successful not only as an example of urban heritage preservation carried out in a way that retains the density required by the CBD location but also as a template for leveraging the commercial value of the office buildings to carry out refurbishment in a situation where financing would probably not otherwise have been available. The theme of adaptive reuse is further strengthened – currently, a separate, rather anachronistic 70s-era building located nearby is also now undergoing refurbishment as opposed to demolition.

6. How can the real estate industry balance the demand for affordable housing with the need for sustainability?

It’s a common misconception that a building can’t be both affordable and sustainable. Affordable housing runs on thin margins, so meeting sustainability goals can require getting creative with funding, financing, and strategy. Depending on the regulatory environment of the locale – the availability of grants, incentives, technology, etc. – the level of difficulty would vary. Often, affordable housing runs on a master utility meter – so when the building reduces energy costs, it’s the owner who benefits from the savings. Residents benefit from higher performance and healthier living spaces, while owners benefit from lower operating expenses. District heat networks can bring similar benefits.

Another approach could be to view housing as part of a larger set of systems of mobility, access to jobs and services, and urban infrastructure. Energy, water, and food systems need to be considered as enablers for affordability, and in a context that enables liveability and equity for everyone who connects with it. All industry players should consider how affordable housing can be more than an independent goal – and explore how it can also contribute to a greener community in the long run.

7. How can the industry engage with and address the concerns of local communities when it comes to sustainable real estate development?

One of the pillars of sustainability is social – i.e., the well-being of the communities in which an organisation operates, or in this case, where the real estate project is being set up. Collaboration across the real estate value chain is proving essential to achieving global sustainability goals. This collaboration includes real estate working alongside governments, community members, tenants, and supply chains. It is an indication that the social element of ESG is genuinely being addressed. This engagement also ensures that new development’s amenities serve the needs of the local community – sometimes developers’ assumptions do not match actual desires.

One emerging topic is to view building utilisation as a solution to sustainability in the built environment. For instance, developers can explore how the surrounding community can use spaces to avoid duplication of amenities that already exist in an area, thereby optimising resources to create more diversified facilities and adaptable spaces. It goes without saying that directly engaging local communities to exchange feedback and address their concerns, such as through dialogue or briefing sessions, should also be of importance. This could mean, for example, carving out space on site for an open park, providing a community food garden (agrihoods), or adding additional EV charging parking spots.

8. What role do you see public-private partnerships playing in advancing sustainability in the real estate sector?

Public-private partnerships (PPPs) can play a significant role in advancing sustainability in the real estate sector by combining the strengths and resources of both the public and private sectors. Private sector expertise and capital can be leveraged to address sustainability challenges that may be too complex or costly for the public sector to tackle alone. On the other hand, governments can help mitigate risks for developers; this, in turn, raises their willingness to invest in sustainable development. This way, the sharing of risks between both parties can produce win-win outcomes in PPP projects.

One such example in Singapore is Eco@Punggol (pictured above), Singapore’s first eco-town. The award-winning project was initiated by the Housing Development Board (HDB), Singapore’s public housing authority, in partnership with various private sector companies. The eco-town features a range of sustainable living initiatives and amenities that enable eco-friendly high-rise living, such as effective energy, water, and waste management. The development also includes a comprehensive network of pedestrian and cycling paths, as well as an extensive public transportation system to encourage the use of sustainable transportation options.

9. How can the industry measure and report on its progress towards sustainability goals?

Over the last 10 years, the avalanche of new ESG reporting requirements applicable to real estate has presented a significant challenge. Keeping up has not been easy, even for the most ambitious organisations with the greatest resources to allocate to the area. In addition, there are different views on what must be prioritised, disclosed, against which criteria, for what purpose and whether commitments will stand up to scrutiny.

It is important to understand the purpose of the different ESG frameworks and standards and the intended user of the information – there is no one-size-fits-all standard. Accordingly, an organisation will need to choose the right standards and metrics that appropriately reflect the requirements of their ESG strategy and their overall environmental impact and comply with minimum social standards throughout the entire real estate lifecycle in value and supply chains.

To help industry players navigate the vast selection of different regulations and standards, ULI has created self-assessing questions that organisations can use to map the core issues and foci of their ESG strategy to the required and appropriate standards and regulations. One of the greatest advantages of streamlining measurement and reporting is that it frees up time for action that we know is needed.

Wesley Place image courtesy of Cox Architecture Eco@Punggol image courtesy of HDB

https://brj.com.sg/wp-content/uploads/2023/06/image3-1.png416624EditorEditor2023-06-23 11:00:372023-07-05 14:34:43ESG Takes Centre Stage in Revolutionising Asia Pacific’s Real Estate Industry