Construction markets across Asia Pacific (APAC) entered 2026 in a strong position, but that momentum is now under pressure following geopolitical disruptions and energy shocks in the first half of the year. The latest Construction Market Insights mid-year report by Linesight revealed that APAC remains among the strongest growth regions for construction, supported by investment in digital infrastructure, advanced manufacturing, energy, transport, and major public programmes.

Most markets within APAC experienced an expanded construction output in 2025 and are on track to sustain this positive trajectory this year. In particular, Malaysia is anticipated to lead growth in the APAC region in 2026, with a projected 6.5 percent increase in construction output. Other Southeast Asian markets are also demonstrating robust growth, with Singapore and Thailand expected to deliver an increase of 4.5 percent and 3.7 percent in construction output respectively.

While demand remains strong, risks in project delivery are rising as market conditions are increasingly shaped by execution constraints rather than demand, influenced by persistent challenges in labour, supply chains and power availability. In an environment of intensified macroeconomic uncertainty and geopolitical disruptions, supply chains are also facing severe constraints and pressures. The report highlighted that recent tensions in the Middle East have pushed the global supply chain pressure index (GSCPI) to its highest level of 1.82 this year since July 2022.

Key market-specific insights to note for 2026 and beyond include:

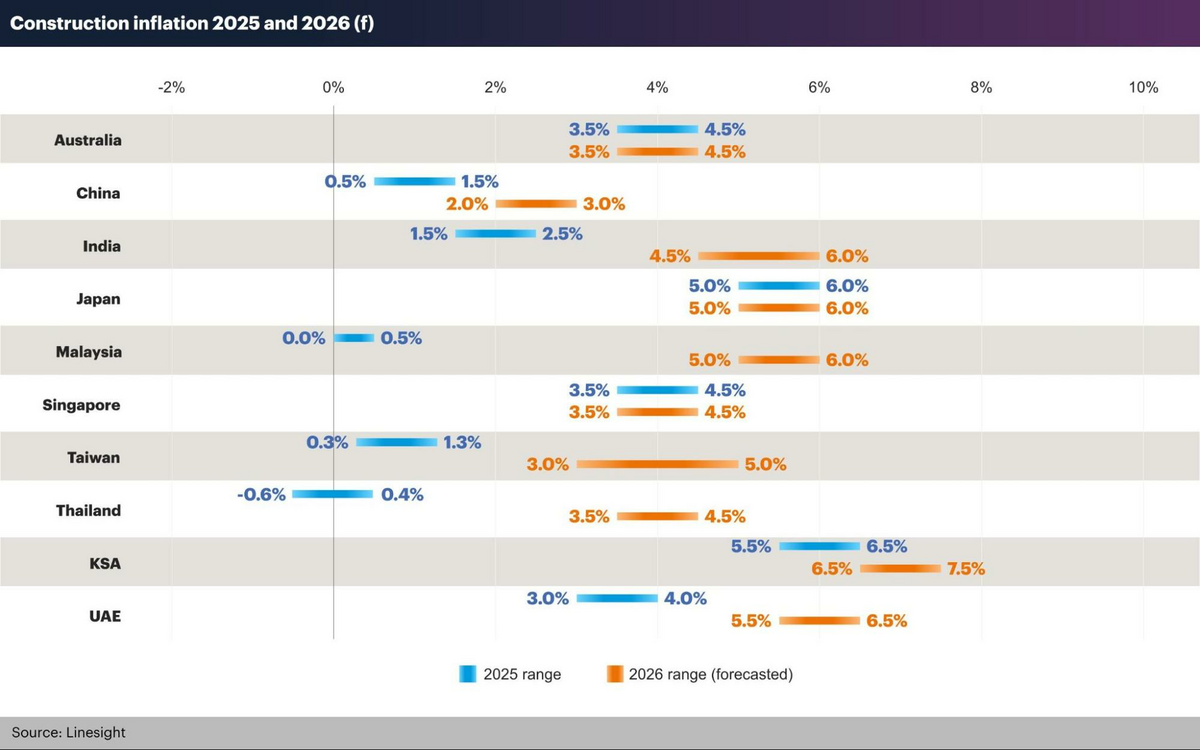

- Malaysia: Construction industry is projected to grow an average of 3.5 percent per year from 2027 to 2030, led by investment in industrial, transport, and energy projects. Construction inflation remains elevated at 5–6 percent, driven by global commodity costs and domestic subsidy and labour pressures. Data centre demand continues to rise, with strong hyperscale interest.

- Singapore: Construction industry is expected to grow around 4 percent annually to 2030, supported by manufacturing and major transport and energy programmes. Construction inflation forecast is 3.5 to 4.5 percent this year, with import reliance exposing the market to conflict-driven pressures. Resource constraints are intensifying, pushing contractor pricing higher amid large projects like Changi T5 and Marina Bay Sands expansion that are moving forward at pace.

- Thailand: The construction industry is recovering steadily, with a 4.3 percent annual growth forecast from 2027 to 2030, driven by data centres, clean energy, and smart industrial estate projects. Construction inflation is also expected between 3.5 to 4.5 percent, reflecting global commodity pressures and domestic labour constraints amid rising data centre demand.

- India: India’s construction industry expanded by 7.2 percent in 2025 and is set for continued growth in 2026. India now leads the APAC region in data centre development, supported by a pipeline valued at US$114bn.

Construction cost inflation across APAC remained elevated through the first half of 2026, though conditions may moderate in the second half provided the Middle East conflict settles. Key commodity prices are facing upward pressures and remain highly sensitive and contingent on the extent and duration of the Middle East conflict. Copper prices rose sharply in Q1 2026 across APAC markets, by 9 percent to 18 percent quarter-on-quarter. In Q2 2026, copper prices are expected to rise by 1 percent to 6 percent, but the likes of Singapore and Malaysia are likely to experience the lower end of this range.

Costlier and longer procurement timelines are also adding to delivery risk. In 2026, lead times for critical long-lead equipment (LLE) globally remain significantly extended. Some have more than doubled since 2021. Based on Linesight’s estimates, cost indices of major equipment categories globally will also increase from a baseline of 1.00 in Q1 2024 to a forecasted 1.08 to 1.19 by Q4 2026.

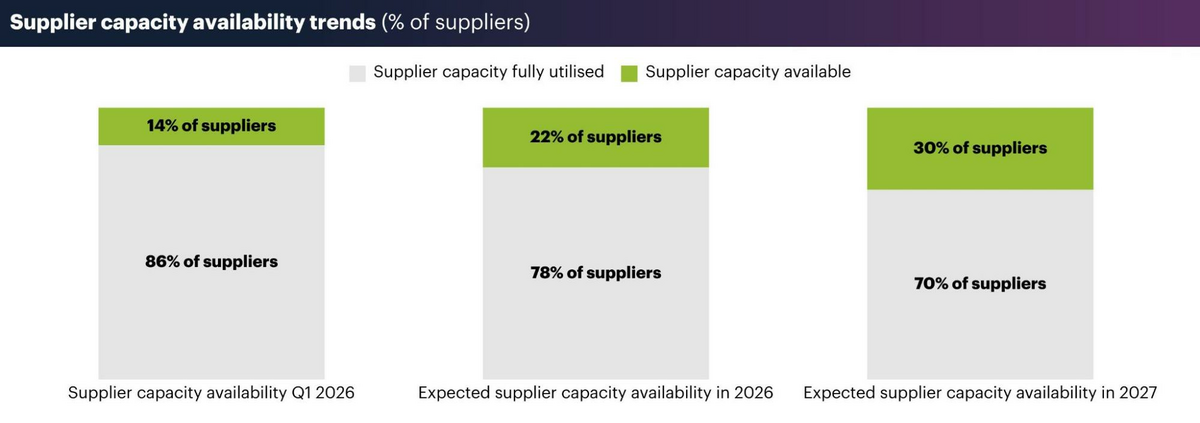

A new chapter in this report is supply chain analysis. Linesight surveyed suppliers across the global data centre supply chain, revealing that 25 percent of suppliers are already operating above 80 percent capacity utilisation. By 2027, 50 percent of suppliers expect capacity utilisation to exceed 80 percent, and more than half are expecting further increases in utilisation from current levels.

Scott Halyday, Regional Director, Southeast Asia at Linesight, said: “APAC continues to be a leader in the global construction market, with data centre demand serving as a key driver of regional growth. As geopolitical disruptions and macroeconomic uncertainty persisted and intensified in the first half of 2026, delivery risk has become the industry’s most pressing challenge to navigate. Earlier planning, more disciplined procurement, and careful contractor selection is becoming increasingly important.”